Industry reports

Polluters pay? The cost of South Australia's algal bloom and who should pay

Year - 2026 Partners - Conservation Council South Australia

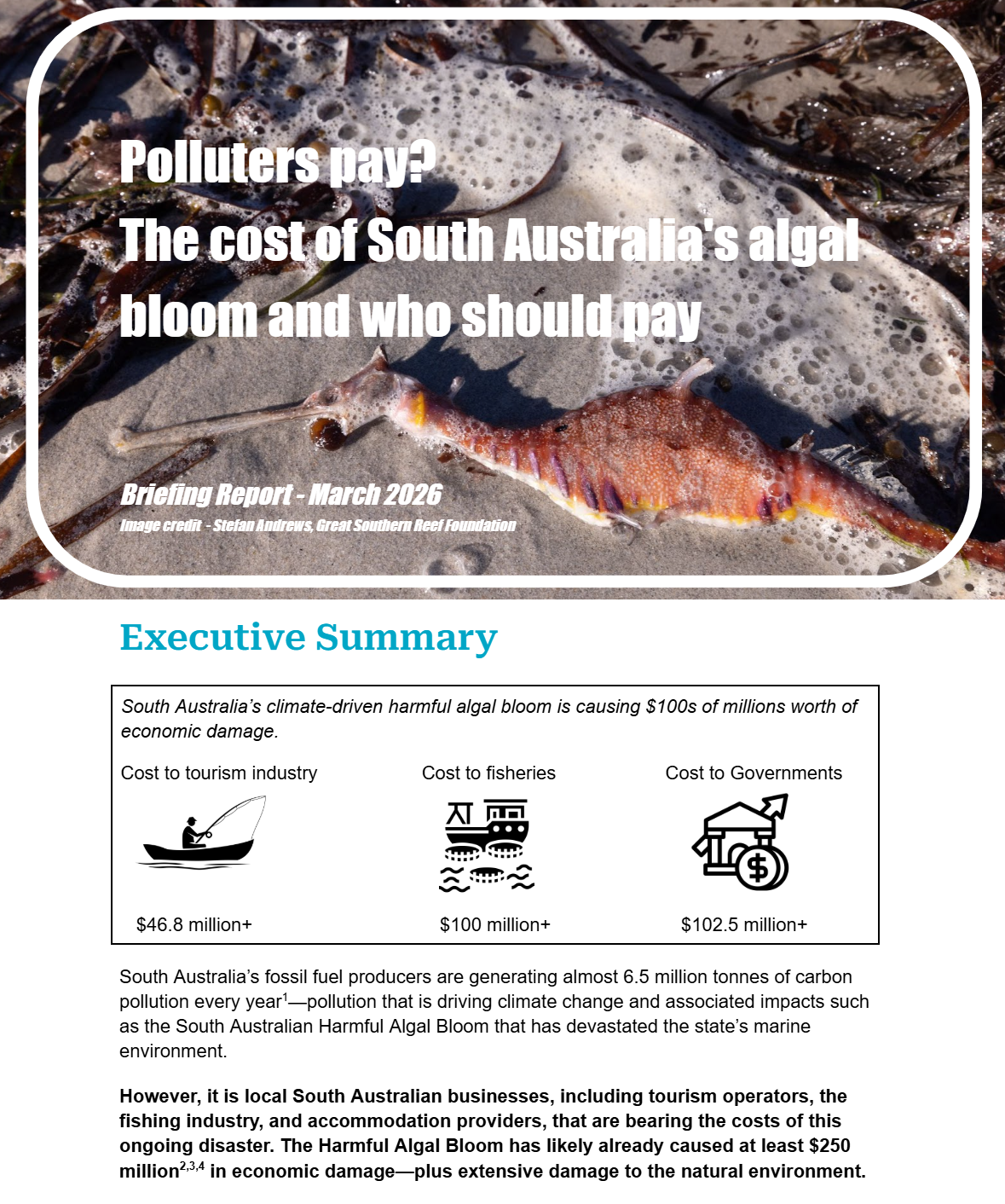

South Australia’s fossil fuel producers are generating almost 6.5 million tonnes of carbon pollution every year—pollution that is driving climate change and associated impacts such as the South Australian Harmful Algal Bloom that has devastated the state’s marine environment.

However, it is local South Australian businesses, including tourism operators, the fishing industry, and accommodation providers, that are bearing the costs of this ongoing disaster. The Harmful Algal Bloom has likely already caused at least $250 million in economic damage—plus extensive damage to the natural environment.

The biggest fossil fuel producers in South Australia profit from the sale of polluting oil and gas products that are driving the disaster—making more than $10 billion in revenue last financial year. According to the Australian Taxation Office (ATO), local fossil fuel producers, despite the multi-billion dollar revenue, paid income tax equivalent to just 0.9% of income.

Similarly, annual royalties paid by the sector to the SA government are unlikely to cover even half the cost of the damage incurred. While there are no State or Federal government policy measures in place to ensure oil and gas producers pay for the damage their polluting products are causing to the marine environment and affected industries, the sector has the wherewithal to compensate those affected. The ‘polluter pays’ principle is an accepted framework for considering who should pay for the costs of environmental damage. In the case of damage caused by climate-linked events—such as those associated with the Harmful Algal Bloom—there is a credible case for South Australia’s largest gas and oil polluters to contribute to the costs of clean up and economic relief to affected industries.

An Algal Disaster Charge of $2.50 per GJ of fossil fuel production in South Australia or a charge of 15% of the assessed value of fossil fuels extracted from the state could raise between $254 million and $275 million per annum. This would compensate for the economic damage and public costs caused so far by the algal bloom.